The Rise of Pay-Per-Mile Insurance and Who Benefits Most

Let’s be honest—car insurance has always felt a little… unfair. You pay the same premium as your neighbor who commutes two hours a day, even if you work from home and only drive to the grocery store. That’s the old model. But there’s a new kid on the block, and it’s shaking things up: pay-per-mile insurance. It’s exactly what it sounds like—you pay based on how much you actually drive. No more subsidizing the road warriors. No more flat rates that ignore your real habits. And honestly, for a lot of people, it’s a game-changer.

So, how did we get here? And—more importantly—who actually saves money with this stuff? Let’s dive in.

What Exactly Is Pay-Per-Mile Insurance?

Pay-per-mile insurance (also called usage-based insurance, or UBI) flips the traditional premium model on its head. Instead of a fixed annual or monthly rate, you pay a small base fee—usually covering things like theft, vandalism, and liability—plus a per-mile charge for every mile you drive. Think of it like a cell phone plan: you have a base rate, then you pay for data usage. Here, the “data” is miles.

Most insurers use a small device plugged into your car’s OBD-II port (that’s the diagnostic port under the dashboard) or a smartphone app to track mileage. Some even use GPS, though that raises privacy questions we’ll touch on later. The key point? Your premium fluctuates with your driving—not with your age, credit score, or zip code.

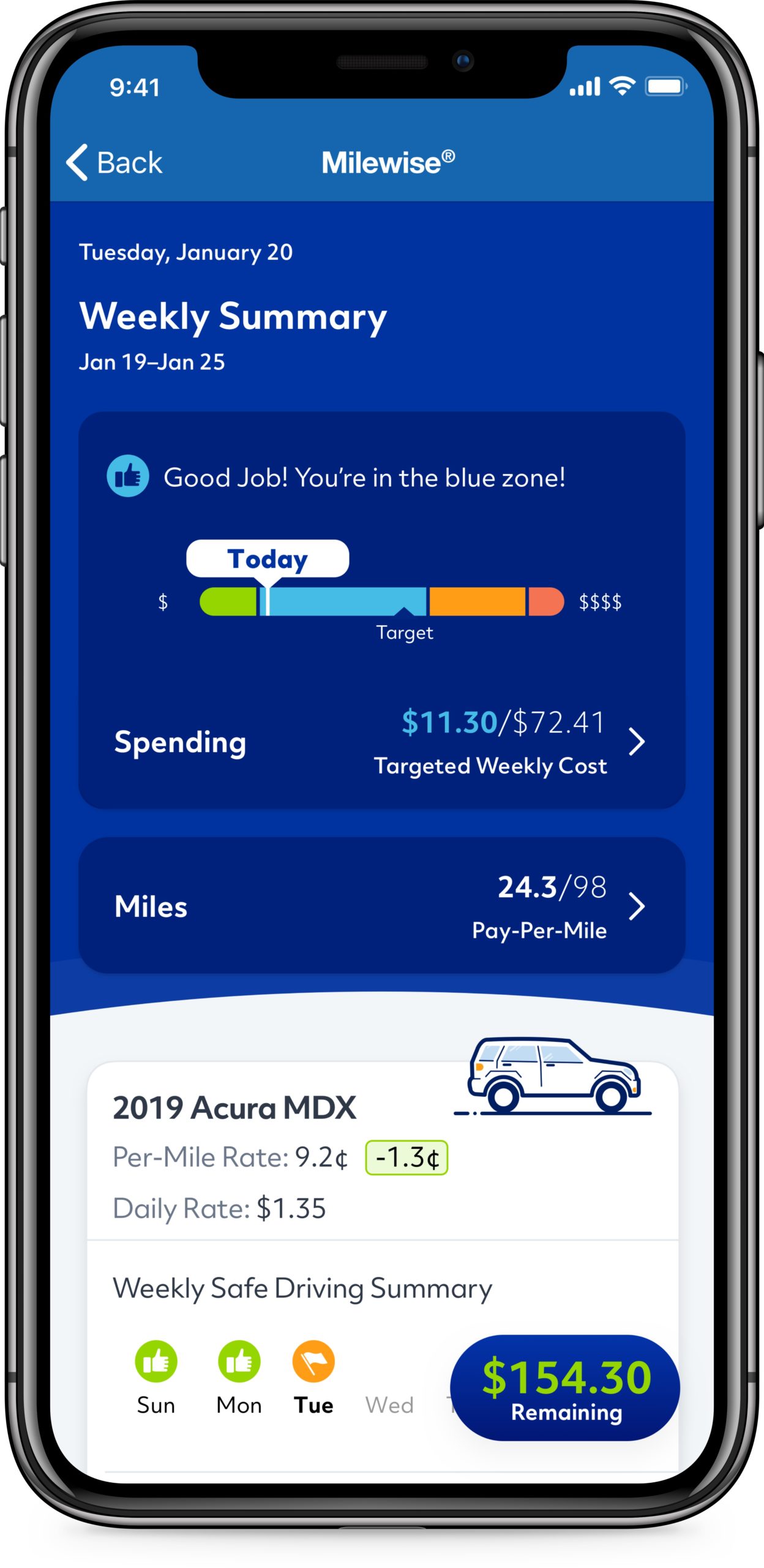

It’s not a new idea, sure. Progressive’s Snapshot and Allstate’s Milewise have been around for years. But the real rise? That’s happening now. Why? Because remote work, inflation, and a cultural shift toward driving less have made people question why they’re paying for miles they never drive.

Why Now? The Perfect Storm for Pay-Per-Mile

You’ve got to look at the timing. Post-pandemic, millions of people realized they don’t need to commute daily. Hybrid schedules are the norm. And gas prices? Well, they’ve been a rollercoaster—so driving less became a financial survival tactic. Suddenly, the old insurance model felt like a tax on the non-commuter.

Add in the rise of telematics technology—cheaper, more accurate tracking devices—and you’ve got a recipe for disruption. Insurers can now measure risk more precisely. And consumers? They’re demanding fairness. Honestly, it’s a win-win on paper. But the real question is: who actually benefits?

The Low-Mileage Driver (Your Classic Winner)

This is the obvious one. If you drive less than 10,000 miles a year—and especially if you’re under 7,000—you’re probably overpaying with traditional insurance. Think about it: retirees, stay-at-home parents, remote workers, and city dwellers who rely on public transit but still own a car for weekends. For these folks, pay-per-mile can slash premiums by 30% to 50% or more.

I’ve seen cases where someone driving 5,000 miles a year saved over $600 annually. That’s real money—like, a nice dinner out every month. But here’s the catch: if you suddenly take a road trip, your bill goes up. So it rewards consistency.

Young Drivers and Students

Young drivers—especially teens and college students—get hammered by high premiums. It’s not their fault; it’s actuarial tables. But if a student only drives to campus and back (maybe 3,000 miles a year), pay-per-mile can be a lifesaver. Some insurers even offer discounts for good driving behavior tracked via the app. That’s a double win: lower rates and a nudge to drive safer.

Sure, there’s a privacy concern—parents might not love the idea of their kid being tracked. But honestly, for many families, the savings outweigh the creep factor. Plus, it teaches young drivers to be mindful of mileage.

Who Else Benefits? The Surprising Groups

It’s not just the obvious low-mileage crowd. Let’s look at some unexpected winners.

- Urban dwellers with a car for emergencies. You know the type—lives in a walkable city, owns a car for trips to IKEA or visiting family. They might drive 2,000 miles a year. Traditional insurance? They’re subsidizing everyone else. Pay-per-mile? They pay peanuts.

- Seasonal drivers. Snowbirds who spend half the year in Florida and half up north. If you only drive six months a year, why pay full premiums for the other six? Some pay-per-mile policies let you pause coverage or just pay the base fee when the car’s parked.

- Households with multiple cars. If you have a “beater” car that only gets used for short errands, you can insure it on a pay-per-mile plan while keeping traditional coverage on the family SUV. Smart, right?

- People with poor credit. Traditional insurance often penalizes bad credit. Pay-per-mile focuses on mileage, not your FICO score. That’s a huge deal for folks who’ve had financial hiccups.

But—and this is important—it’s not for everyone.

Who Should Think Twice (Or Run the Other Way)

Pay-per-mile isn’t a magic bullet. If you’re a high-mileage driver—say, a sales rep logging 20,000 miles a year—you’ll likely pay more than a traditional policy. The per-mile charges add up fast. Also, some insurers cap the maximum miles or charge higher base fees in high-risk areas. So do the math.

Then there’s the privacy angle. Not everyone loves the idea of their insurer knowing exactly where they drive, when they drive, and how fast. Some policies use GPS; others just track mileage. Read the fine print. If you’re a privacy hawk, you might prefer a traditional plan or a “black box” that only records odometer readings.

And here’s a weird one: if you’re a very low-mileage driver—like under 1,000 miles a year—you might actually be better off with a classic “pay-as-you-go” policy or even dropping comprehensive coverage. Sometimes the base fee alone isn’t worth it. Yeah, it’s a niche problem, but it’s real.

How to Decide if Pay-Per-Mile Is Right for You

Here’s a simple framework. First, estimate your annual mileage. Check your odometer from last year’s oil change. If it’s under 10,000, you’re in the sweet spot. Under 7,000? You’re probably leaving money on the table.

Second, compare quotes. Most major insurers now offer a pay-per-mile option. Get a traditional quote and a usage-based quote side-by-side. Look at the base fee and the per-mile rate. Some companies charge 5 cents per mile; others charge 10 cents. It varies wildly.

Third, check for caps. Some policies have a daily or monthly mileage cap. If you exceed it, you get charged a flat rate—which might negate the savings. Ask about “maximum miles” clauses.

Finally, think about your driving habits. Do you take spontaneous road trips? Do you drive late at night? Some policies adjust rates based on time of day (riskier hours cost more). That’s fine if you’re a daytime driver, but night owls might get stung.

The Bigger Picture: Is This the Future?

Honestly, I think pay-per-mile is just the beginning. We’re moving toward a world where insurance is hyper-personalized. Think about it: with electric vehicles, autonomous driving, and car-sharing services, the old model of “one size fits all” feels archaic. Pay-per-mile is a stepping stone to even more granular pricing—like pay-per-minute or pay-per-trip insurance.

But there are wrinkles. Regulators are still catching up. Some states have restrictions on usage-based insurance. And there’s the equity question: if low-income drivers tend to drive less (because they can’t afford gas), pay-per-mile could actually be a progressive tool. But if they live in high-risk areas with high base fees, it might not help. It’s complicated.

Still, for the average person who drives less than 10,000 miles a year—which, by the way, is about 40% of U.S. drivers—pay-per-mile is a no-brainer. It’s fairer, more flexible, and surprisingly easy to set up. You just plug in a device or download an app, and you’re off.

Final Thoughts (No Sales Pitch)

Pay-per-mile insurance isn’t a revolution—it’s an evolution. It’s the industry finally catching up to how we actually live. For some, it’s a lifeline. For others, it’s a gimmick. But one thing’s for sure: the days of blindly paying for miles you never drive are numbered. So, take a look at your odometer. Do the math. You might be surprised at what you find.

And hey—if nothing else, it’s a good excuse to drive a little less. Your wallet (and the planet) might thank you.